Article

How to strengthen GAP insurance performance in affordability-challenged markets

Pricing and monitoring GAP for sustainable performance

GAP insurance has always served a straightforward purpose: Protect the customer from owing more than their vehicle is worth in a total loss. What’s changed is the market surrounding it, and that shift demands a more strategic approach to how dealers price, structure, and monitor their programs.

The gap between what buyers owe and what their vehicles are worth is widening. In Q1 2026, roughly 30% of trade-in borrowers entered new loans with negative equity, carrying an average shortfall of $7,200 — up 42% from five years ago.1

Total losses are happening more frequently. The financial exposure per claim keeps climbing. For dealers, the real question is whether today’s customers can afford to go without GAP protection and whether your GAP strategy is built for today’s market.

Why GAP exposure is growing on two fronts

GAP performance is shaped by two core variables: severity (how large the gap is when a claim occurs) and frequency (how often total losses happen). Both are moving in directions that increase risk.

Severity is climbing.

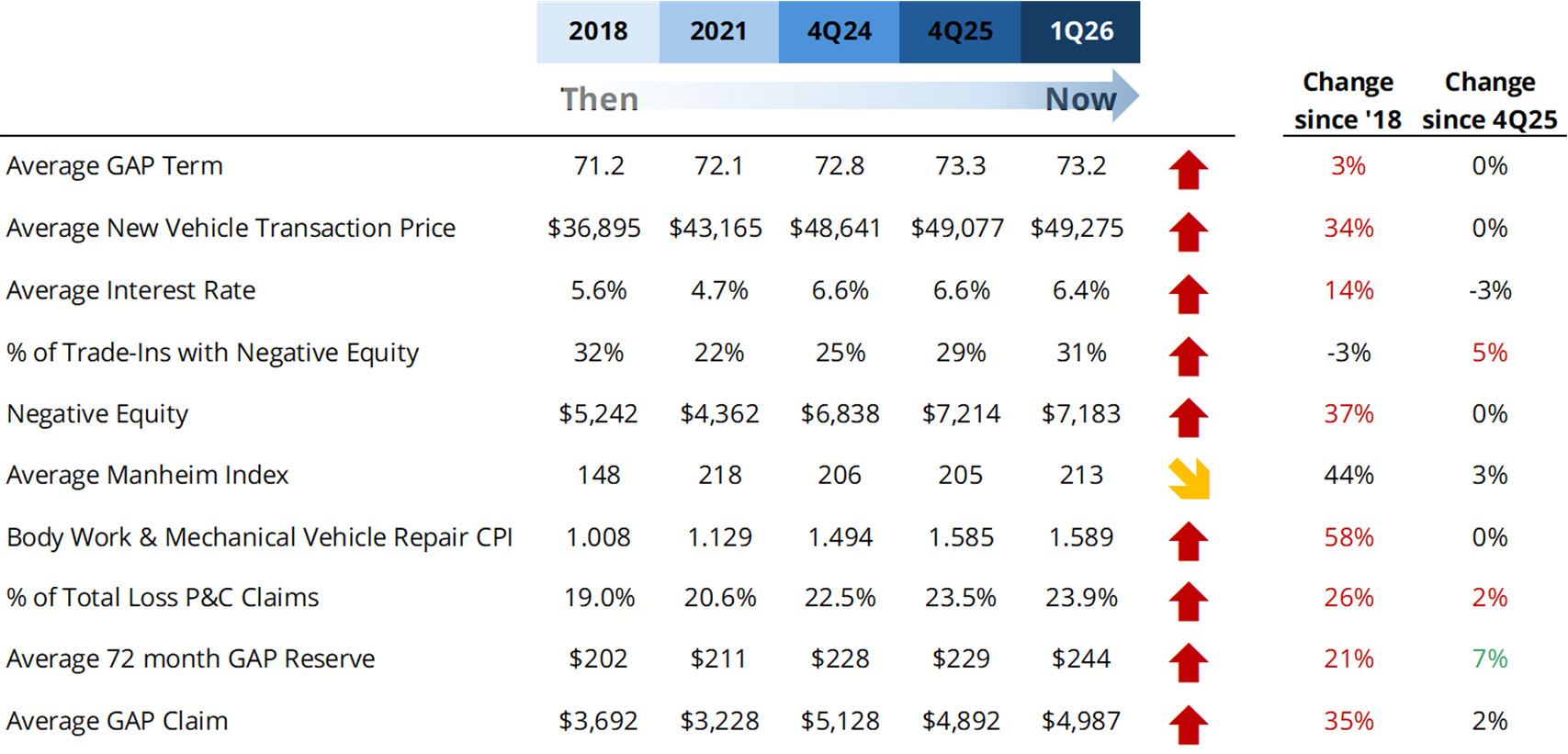

New vehicle transaction prices reached an average of $49,461 in April 2026, up 0.4% over the previous month and +1.3% year over year according to Assurant’s own internal GAP data.2 Our Q1 report showed even more signals of increasing severity.

- GAP in amounts financed: The average new car loan was roughly $33,4723 in Q2 2019, which has grown to $43,5824 in Q4 2025.

- All-time-high negative equity: Negative equity on new car trade-ins averaged $7,183 in Q1 2026, fairly steady with Q4 2025's figure of $7,214, and still up 37% since 2018. At the end of the quarter, 31% of trade-ins carried negative equity.

- Stretching loan terms: Per Edmunds Q3 2025 data, terms continue pushing to 72, 84, and 96 months, slowing principal paydown and keeping buyers underwater longer.

- Elevated claim costs: The average GAP paid claim rose to $4,987 in Q1 2026, reflecting the structural widening between loan balances and vehicle values.

GAP losses are structurally higher today than in prior cycles: When losses last peaked in 2018, average severity was $3,692 alongside a negative equity high. Compared that to roughly $5,000 today, and it's a 35% increase, with no clear indication that negative equity has yet reached its peak.2

Frequency is rising.

When repair costs exceed vehicle value, insurers total the vehicle. That threshold is being reached more often. Internal Assurant data in the chart above shows total loss rates matched a record high of 23.9% of claim counts in Q1 2026, driven by rising repair costs, an aging vehicle mix, and increasing technology complexity, particularly ADAS systems, sensors, and EV components that make even moderate damage expensive to fix.

Higher frequency and higher severity together mean more claims, and costlier ones. For dealers, this changes the economics of GAP in ways that require active management, not passive participation.

The dealer reality: why GAP strategy impacts more than F&I

Front-end margins keep tightening, and F&I income carries greater weight in overall profitability. GAP is a core revenue driver, but treating it as a set-it-and-forget-it product introduces risks that surface downstream.

Pricing discipline matters. GAP priced too aggressively may win short-term volume but creates adverse claims development that erodes program stability. When loss ratios deteriorate, consequences show up in reinsurance profits, future pricing, and confidence in the F&I portfolio. Pricing informed by strong actuarial data protects profitability over time.

GAP can strengthen the financing conversation. In a market where many buyers are putting minimal down payments on extended terms, GAP may be a factor in securing financing or more favorable loan terms. Lenders recognize the risk profile of high-LTV deals, and protection that mitigates that exposure supports the overall deal structure for both dealers and buyers.

Customer trust is at stake. GAP that’s clearly explained and fairly structured reinforces the dealership’s role as a buyer advocate. That trust extends beyond the initial sale: Customers who feel protected are more likely to return for service, enroll in prepaid maintenance, and recommend the dealership. Those who feel oversold or discover inadequate coverage at the worst moment are less likely to come back.

The customer reality: stretched buyers need protection, not pressure

These buyers aren’t theoretical. Stressed consumers are in dealerships today, financing vehicles with high LTV ratios, extended terms, and limited equity cushion. Auto loan delinquencies of 90 or more days reached 2.97% in Q1 2026.2 Used vehicle values remain materially below their 2022 peaks,5 which means vehicles purchased during the price spike now carry disproportionate negative equity.

Dealers who frame GAP as an essential part of the transaction, one that supports the buyer's financial position, build credibility at a moment when buyers are most alert to whether the dealership is working in their interest.

The outlook for the rest of 2026: elevated risk, emerging opportunities

GAP losses will remain elevated through 2026, though claims are showing signs of normalization.

- Negative equity will persist. Higher rates, longer loan terms, lower down payments, and used vehicle depreciation have driven negative equity averages to all-time highs. This structural condition won’t reverse quickly.

- GAP paid claims are increasing: The average GAP paid claim increased in 2026 Q1 to $4,987, up 2% from the 2025 Q4 average of $4,900.2

- Total loss frequency will likely remain elevated. Lower used vehicle values, increased labor and parts costs, an aging vehicle mix, and added technology complexity all push more vehicles past the repair-versus-replace threshold.

- Interest rate movements will matter. Higher rates prolong GAP exposure by keeping outstanding loan balances elevated. As of Q1 2026, average interest rates were 6.4%, only a 0.2 decrease from a 6.6% high in 2024 and 2025.2Any rate relief in 2026 could reduce exposure on new originations, but existing portfolios will reflect current rate conditions for years.

- Tariff-driven pricing is likely here to stay. As we’ve seen with other pricing increases tied to inflation and supply chain disruption, downward adjustments tend to be small, if they happen at all. For GAP, this means elevated loan values on vehicles purchased at tariff-inflated prices will persist, extending risk exposure.

This environment rewards proactive GAP management. Maintaining the status quo on GAP pricing and relying on trailing assumptions can lead to unexpected program deterioration that doesn’t get noticed until the damage is already done.

How partnership helps swing GAP back in your favor

GAP performance depends on variables that shift constantly: vehicle values, loan structures, claims patterns, and repair cost trends. Managing those variables well requires actuarial depth, not just competitive pricing. The critical question for dealers is whether their provider has the data foundation and discipline to price GAP for sustainable performance rather than short-term edge. That means multiple years of claims history informing current models, continuous monitoring of emerging frequency and severity trends, and the willingness to adjust proactively before deterioration shows up in a dealer’s results.

Questions worth asking your GAP provider

The dealers managing GAP most effectively are asking specific questions of their providers.

- Are you adjusting pricing assumptions to reflect current market conditions, including vehicle value trends, loan term shifts, and claims development?

- What conservatism is built into your underwriting, and how does it protect my program from unexpected claims deterioration?

- What reporting do I receive to monitor program performance, and how frequently is it updated?

- How do you identify and communicate emerging claims trends before they impact my results?

- Is your pricing strategy optimized for sustainable performance or for short-term competitiveness?

Building GAP strategy for the market ahead

Dealerships that manage GAP most effectively treat it as a strategic capability: relevant to today's deal structures, transparent in how it works, and backed by a partner that can keep pace with changing risk dynamics. When the gap widens and losses happen more often, the value of getting this right becomes visible across the entire business, from F&I performance and reinsurance health to customer retention and long-term profitability.

Assurant leverages deep actuarial knowledge, robust datasets, and advanced modeling tools to provide partners with the insight needed to navigate volatility. Our approach delivers the transparency and discipline required to reduce risk and maximize performance.

Start your free profit analysis today.

References

- Wall Street Journal, America’s Pandemic Car Bubble Is Now Trapping Buyers in Debt, April 25, 2026 (https://www.wsj.com/business/autos/car-owners-debt-negative-equity-3cfcd031?AutomotiveVentures)

- Assurant, Global Automotive GAP Report, Q4 2025

- Edmunds industry insights, December 2019

- Experian State of the Automotive Finance Market, Q4 2025

- Cox Automotive, Manheim Used Vehicle Value Index, Dec. 2024